US $2.2Trillion Post GFC Stimulus

That is a lot of money and most of it went straight to the US banks as Quantitive Easing stimulus. Have the American people seen any of that stimulus money? Have American businesses seen any of that stimulus money? I doubt you could find any that could answer those questions in the affirmative. So where did it go?

Well, thanks to this article (please read it afterwards) by Ilargi published yesterday on The Automatic Earth website, I now understand a little better what has occurred.

The article contains some very revealing graphs on the results of US govt QE policy over the last few years since the GFC and why the injection of over $2 Trillion into the economy of that nation has made little or no difference. Ilargi provides some insightful deliberations on these matters.

Most of the graphs accompanying the article are interesting in their own right and could be usefully considered at some length for their informative nature. However, the purpose of my post is simply to show just what is revealed in answer to my initial question of where that money went. At least, answered to my own satisfaction.

Just Where Did That Money Go, And Why?

Thanks to Illargi’s work and also to the graph provided in the first comment on the article, I now have a fair understanding as to just where that $2T has gone.

The short answer is: Nowhere. At the very most it has only journeyed (electronically of course since it doesn’t actually or physically exist):

a) from the Fed (US Federal Bank) to the coffers, sorry, I meant computers, of the US commercial banks

and then

b) from those banks back to the Fed, in the form of banking reserves, as interest earning deposits.

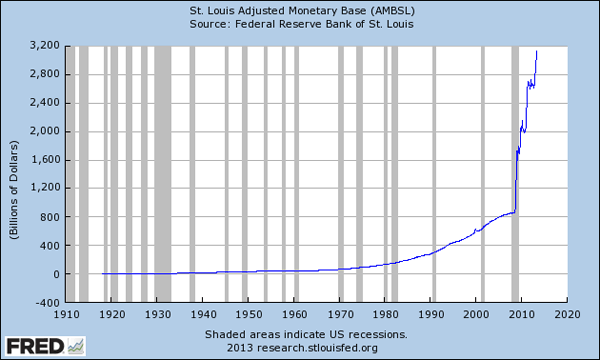

From the following graph, used in the article, it can be seen that the Monetary Base (the sum of currency circulating in the public plus the commercial banks’ reserves with the central bank, the Fed) was tracking along nicely for many years until the GFC in 2008. From that time it has jumped dramatically by several trillion dollars in a number of stepped leaps that coincide with the Fed’s QE releases of stimulus.

The QE steps are more pronounced in the graph below, also extracted from the article, since it covers a much smaller period and in fact only goes as far as early 2012:

The QE steps are more pronounced in the graph below, also extracted from the article, since it covers a much smaller period and in fact only goes as far as early 2012:

So, that answers where the ‘money’ went. From the Fed, back to the Fed. A fitting situation really since it, the money, never really existed in the first place. All of the ballyhoo about Helicopter Ben Bernanke running the government printing presses to get more dollars into the economy, was just that, ballyhoo.

So, that answers where the ‘money’ went. From the Fed, back to the Fed. A fitting situation really since it, the money, never really existed in the first place. All of the ballyhoo about Helicopter Ben Bernanke running the government printing presses to get more dollars into the economy, was just that, ballyhoo.

There was no printing of money. Just electronic signals running from the Fed’s computers to the banks computers and from the banks computers back to the Fed’s computers.

Maybe Helicopter Ben is not as dumb as he is made out to be. Or maybe he (and others) are much more devious than anyone has given him/them credit for.

OK, the ‘where’ question has been taken care of. What about the ‘why’ question?

For me, the explanation by Dave Fairtex (who he is I do not know, but he regularly comments on TAE and other financial websites) cannot be bettered, so I repeat it here in full, giving him the credit and also credit to The Automatic Earth blog.

“So BASE includes EXCRESNS – Excess reserves deposited at the Fed.

This is essentially cash deposited at the Fed in excess of the reserve requirements. Why do banks deposit anything at the Fed if they don’t have to? The Fed currently pays 0.25%. Currently, a one-year treasury bill pays 0.14%, and short-term bank repos pay about 0.09%. In other words, the Fed is giving Banks a good deal, so guess what – the banks take it.

People aren’t borrowing – enough anyway – so the banks need to make money in order to pay their depositors that 0.01% they get from their savings account. So, banks take deposits, pay 0.01%, and get 0.25% from the Fed. It won’t make them rich, but its better than nothing, that’s for sure.

Anyone – how much does your money market fund pay you? How much does your savings account pay you? If you could get 0.25% for ultimately safe deposits, would you take it? I sure would. The Fed is the bank that will never go under!

The Fed started paying for excess reserves in October 2008. Short term treasury bond yields plummeted at that moment as money fled to safe havens, and it was at that moment that excess reserves category took off.

To me EXCRESNS is the place where a big chunk of QE money goes to…well if not die, then sleep. If the Fed decided to stop paying 0.25%, the excess reserves would flee from there into somewhere else that provided yield. Perhaps the 1 year treasury yield would fall even further.

QE does construct a bubble in the bond market, by propping up bond prices, and then most of the cash goes to park at the Fed, back where it started from.”

It should be obvious even to ‘Blind Freddy’, to use an old Aussie colloquialism, that there is a very strong correlation between the EXCRESNS – Excess Reserves Deposited at the Fed (red line) in the above graph and the now obvious leaps in the Money Base (black line) following third quarter 2008 which represent the QE1, QE2 and QE3 stimulus payments to those same banks.

The commentary explanation from Dave Fairtex gives the reason for this process. Not only do the ‘Too Big To Fail’ banks gain the security of the additional federal reserves that they now hold, courtesy of the Fed, but they are also gaining interest of 0.25% from the Fed on those deposits. That may not sound very much gain, but interest on $2 Trillion is not a small amount and again it can clearly be seen that around $1.8T has been deposited with the Fed in the last five years but the Base has grown by around $2.4T. Since the US economy has been at a standstill over this period, a lot of the extra Base Money can only have come from interest earned by the banks from the Fed. Very nice work, if you can get it. The banks are secured, even making some profit without doing anything. Even the profit they are making is much more than they have to give out to their own depositors with interest rates so low. And all this without the government having to print a single dollar.

So, What’s The Plan?

Meanwhile, as Ilargi points out, the money supply, the movement of actual currency floating in the economy, is rapidly declining. The economy is going nowhere in spite of the current buoyancy of the equities market and being talked up by just about everyone.

Something has to give.

If the Federal Bank actually planned for what we are now seeing, what was their objective? Did they mis-calculate how things would turn out? Or is there some more devious plan afoot?

Whatever the case, it does not bode well for the future of the people of the United States and ultimately for much of the rest of the world.

I am, in my various writings, often warning of impending collapse of our social structures at some point in the future. We are heading in the right direction for such events to ultimately overtake us and the US may well be a leader or instigator in triggering something of that nature.

My advice? Always keep one eye firmly on that possibility.

Leave a comment